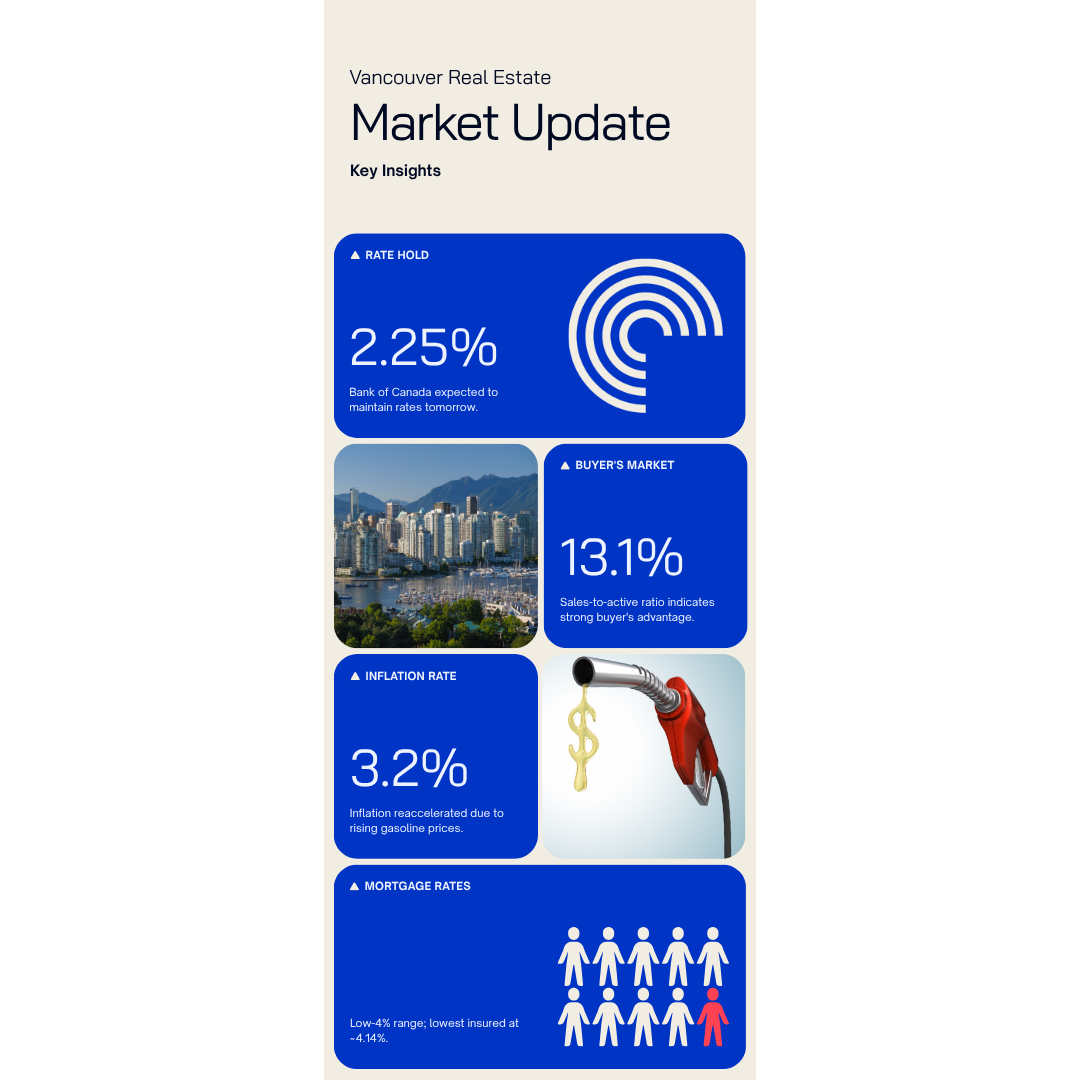

Tomorrow, July 15, the Bank of Canada is widely expected to leave its overnight rate unchanged at 2.25% — the sixth consecutive hold since the cutting cycle wrapped up last October. The headlines will read "no change," and most people will shrug and move on. That's exactly the mistake.

A hold is not a non-event. It's confirmation that the cost of borrowing has found a floor for now, and it removes the single biggest excuse buyers have been leaning on all year: "I'll wait for the next cut." When you understand what's happening underneath that steady rate, the picture in Vancouver looks less like a stalemate and more like an opening.

Here's the backdrop the Bank is wrestling with. Inflation reaccelerated to 3.2% in May, up from 2.8% in April, driven largely by a gasoline surge tied to the ongoing Middle East conflict. Growth, meanwhile, is soft. That combination — hot prices, cool economy — is why a cut isn't coming and why the five-year Government of Canada bond yield is parked around 3.15%. Fixed mortgage rates track that yield, so the lowest insured five-year fixed is still available near 4.14%, with discounted bank rates around 4.9%. Translation: financing is stable, predictable, and not going anywhere fast. For buyers, certainty is a tool you can actually plan around.

Now layer on the local reality. Metro Vancouver is in genuine buyer's-market territory, with a sales-to-active-listings ratio of just 13.1%. Active inventory is running roughly 22% above the 10-year July average. Detached benchmarks have eased to about $2.09 million and downtown condos to around $795,000 — softer than a year ago. By almost every measure, conditions are more favourable to family buyers than they've been in close to a decade.

As someone actively writing offers in this market, I can tell you what those numbers feel like on the ground: buyers are getting subject clauses accepted again, sellers are negotiating on price and timing, and the frantic bidding wars of past cycles are largely absent. As an investor, I read the same data differently — motivated sellers plus stable financing is exactly the setup for acquiring quality assets before sentiment turns.

And it will turn. On the supply side, Ottawa's newly launched Build Canada Homes agency and its BC partnership are pushing factory-built and shovel-ready projects, while BC Builds recently broke ground on some 820 homes in Burnaby. That pipeline matters for the long run, but it won't relieve today's shortage of resale, family-sized homes in established neighbourhoods. When rates eventually do ease, the buyers now sitting on the sidelines will pile back in — and this negotiating room will evaporate.

That's the observer's read on where this is heading: the advantage belongs to people who act while the crowd is distracted by a rate announcement that, frankly, changes nothing about their situation. A steady 2.25% isn't a reason to wait. In this market, it's a green light.

If you've been circling the market, this is the window to get pre-approved, tour seriously, and negotiate hard — while inventory is deep and competition is thin.

Kevin Lynch is a leader in the real estate industry with 36 years of experience in sales, marketing, coaching, training. He is a published author and speaker and has been interviewed in the media many times including TV, Radio, newspapers and magazines.

Thinking about your next move?

Let's talk. | hello@kevinlynch.ca | kevinlynch.ca | 604-307-9448

#VancouverRealEstate #BCHousing #MortgageRates #BankOfCanada #VancouverHomes #RealEstateInvesting #KevinLynch #BCMarket #MetroVancouver #HomeBuyers